Retail Lending Journey

Loan origination is the process by which a borrower applies for a new loan through a request or application form and a lender processes the application. The lending journey generally comprises various stages from submitting a loan application up to disbursal of funds where the request is treated as completed. But there can be exceptions where journeys can complete after going through only a few stages.

Journey Overview

After an application requesting for a retail lending product such as overdraft, personal loan, a credit card or Mortgage loan is submitted by the applicant or a CSR using the Temenos DigitalOrigination (Self Service) application, the submitted request is received in the Temenos Digital Assist solution and processed by the bank users. The data which was originally captured in Origination Data Storage microservice (ODMS) is transferred to Origination Processing microservice after the request is submitted in the Temenos DigitalOrigination application. The Origination Processing MS is enhanced to classify data based on lending journeys using Line of Business attribute. Since the requests will be processed in various stages, the initial stage of the request received in the Assist solution will be Submitted. Every stage has preconfigured (auto) and manual tasks where the bank user with specific user role and necessary permissions is expected to complete the tasks before the request can be sent to the next stage.

The retail lending request goes through the following lending stages:

- Submitted: After a lending request for overdraft or term loan is submitted, the request is received in the Temenos Digital Assist solution and assigned the Submitted stage.

- Prescreening: The Lender screens the customer to determine whether to extend an offer of credit.

- Credit Packaging: The lender calculates the credit worthiness of a business or organization involving financial analysis techniques and a detailed analysis of cash flows.

- Underwriting: Request application is approved or denied.

- Closing: The executed items are reviewed and the request application is boarded to the servicing system for servicing.

The retail lending journey stages and tasks are created and managed in Red Hat Process Automation Manager (PAM) server.![]()

- Auto tasks: System evaluated tasks. In case of auto tasks, the DMN rules engine

evaluates the task criteria and when all the conditions are met, marks the task as completed. These tasks are executed at the back-end and are not visible to the user. In case the evaluation criteria is not met, the auto tasks are failed and come to remedy user for taking action.

evaluates the task criteria and when all the conditions are met, marks the task as completed. These tasks are executed at the back-end and are not visible to the user. In case the evaluation criteria is not met, the auto tasks are failed and come to remedy user for taking action. - The manual tasks are created in PAM but since no data evaluation points are there, these tasks are completed by the bank user always.

After a task is completed, the Process Automation Manager (PAM) processes the data at the back end and makes sure that all the tasks in a specific stage are processed for completion before moving the request to the next stage. For information on the Red Hat PAM flows for the lending applications, click here.

The request is received initially by the Relationship Manager (RM) of a financial institution or bank and further processed by the RM and other bank users (Underwriter, Operations, Supervisor) by completing the tasks assigned to them.

Journey Stages and Tasks

This section explains the lending journey categorized into Automated SME Lending Process and Problem Loan Management (manual process) depending on the type of the applicant.

- Automated Lending Process is enabled for the applications whose applicants are existing customers, provided there is no change in customer data.

- Problem Loan Management Process is enabled for the applications whose applicants are prospects and existing customers with change in customer data.

After the request is received in the Assist solution, the PAM server sends out the auto tasks that are to be performed in each of the stages. The bank users are expected to complete all the assigned tasks before sending the request to the next stage until the request is fulfilled. Each stage has a set of tasks (auto and manual) that are to be completed before the request application is moved to the next stage. For the complete list of tasks created per stage, refer to the enclosed document (compressed file in .zip format).

Automated Lending Process

Automated Process is enabled for the applications whose applicants are existing customers provided there is no change in customer data.

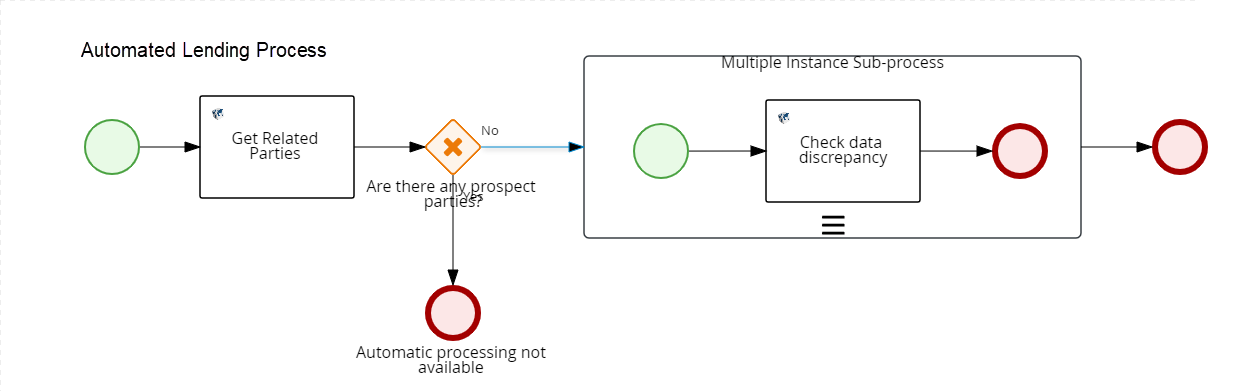

After the request application is submitted Temenos DigitalOrigination (Self Service) application, the system goes through the workflow as shown in the diagram to automate the lending process.

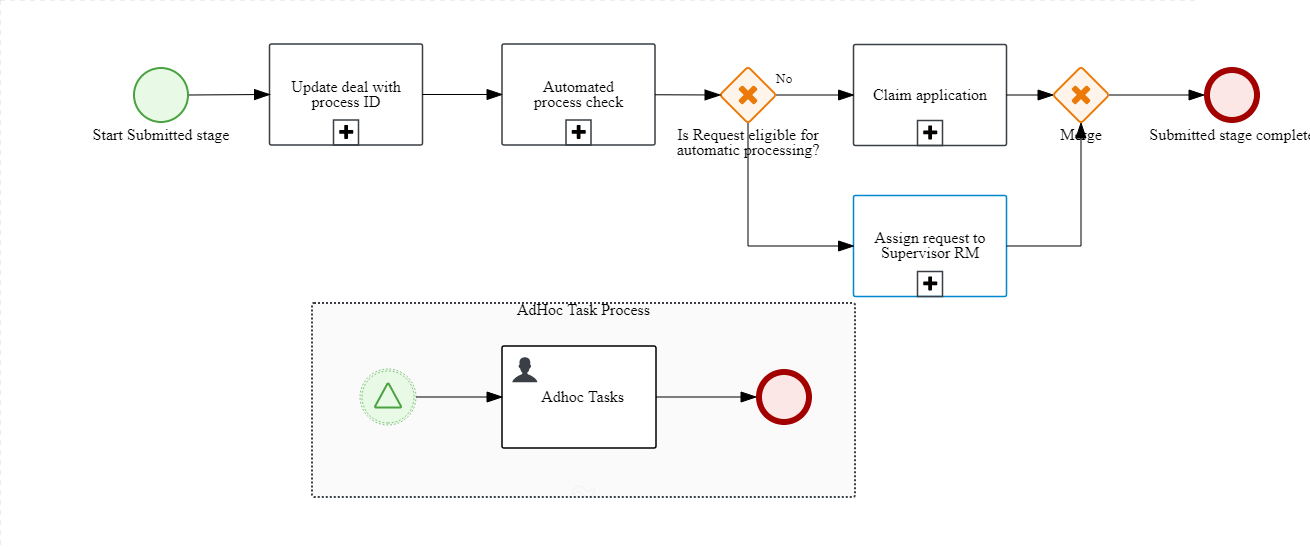

Submitted

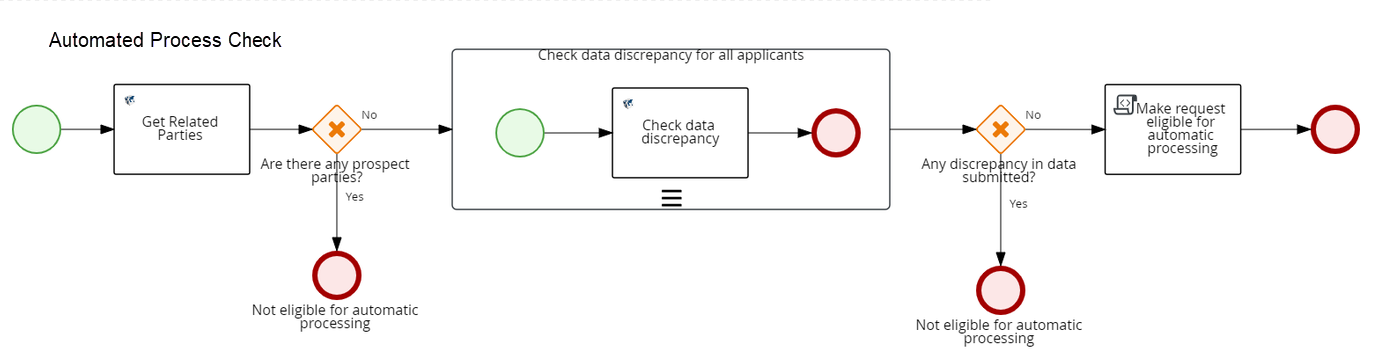

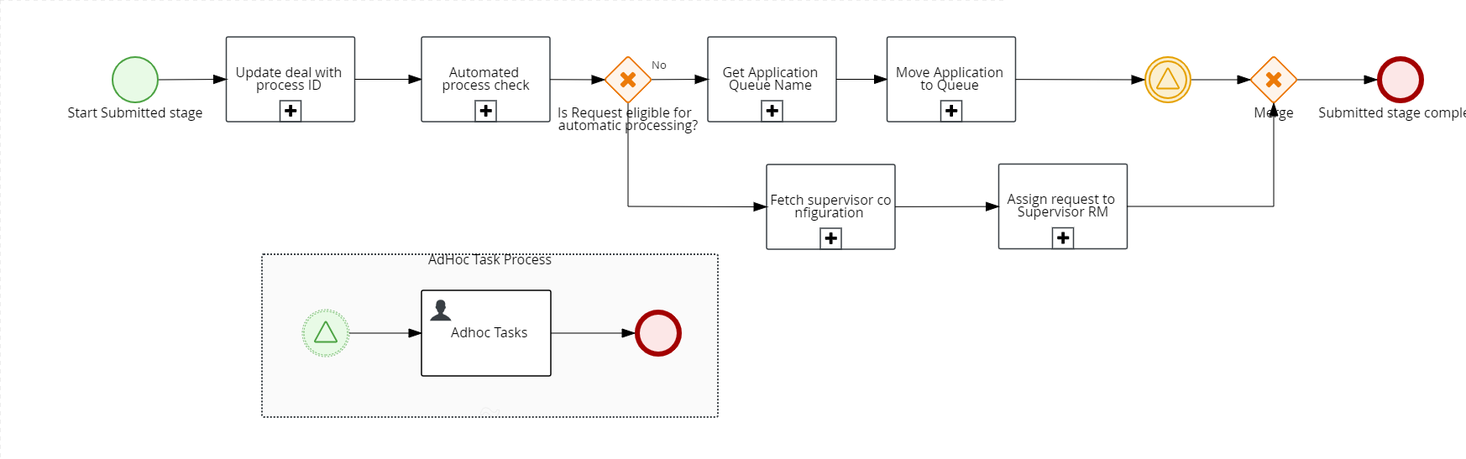

Post submission, the system goes through the following Retail Lending workflow with automated Lending process check. In the automated lending process check, the data in ODMS is compared with that of Party MS. If there is no discrepancy in address, personal, identity, income and employment information, the automated lending flow kicks in. The application is assigned to Supervisor RM and the system processes the next task. Otherwise, if there is any discrepancy in data, then the problem loan management flow kicks in.

Updates deal (application data) with Process ID and automated lending process check is done.

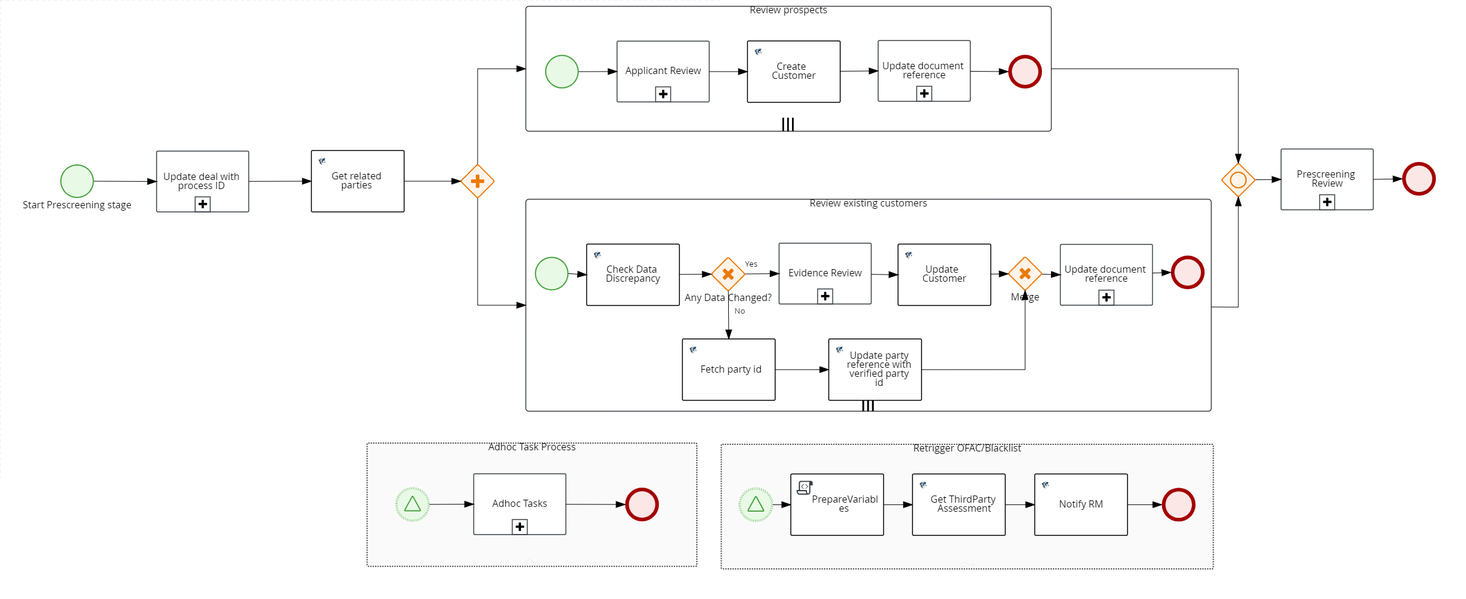

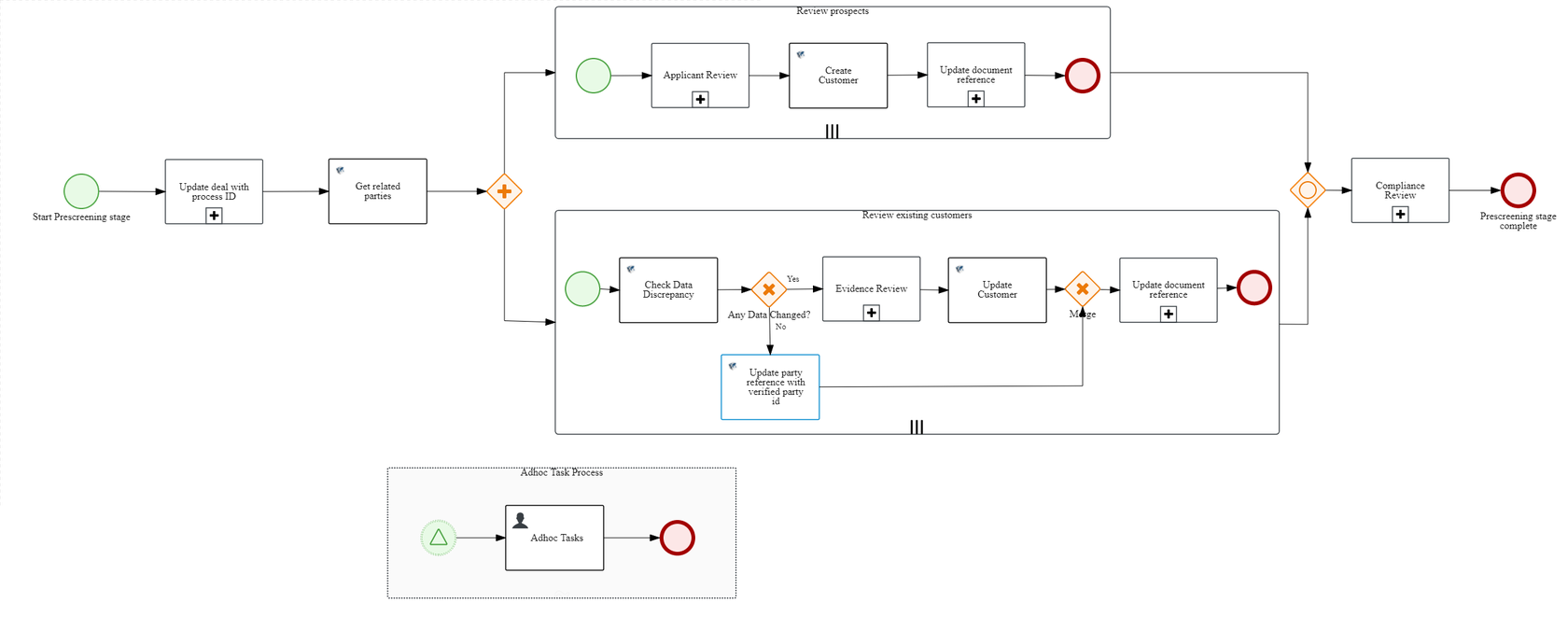

Prescreening

An applicant review task is created for each prospect. All mandatory information required to create a party is reviewed and edited by a Relationship Manager and then a customer id is created in Party microservice and Temenos Transact. If an existing customer applied for a loan, evidence review and then compliance review tasks are created. The customer data will be updated in Party microservice and Temenos Transact.

Review KYC Information

For existing customers, data discrepancy is checked. If the automated lending process is set, then the evidence review is automatically closed.

Review Loan Document

If the flag returned by Automated Lending process check is not set then there is no change in the Income and Employment data and if the status of the Loan documents is Submitted or Verified, then this task should be automatically closed.

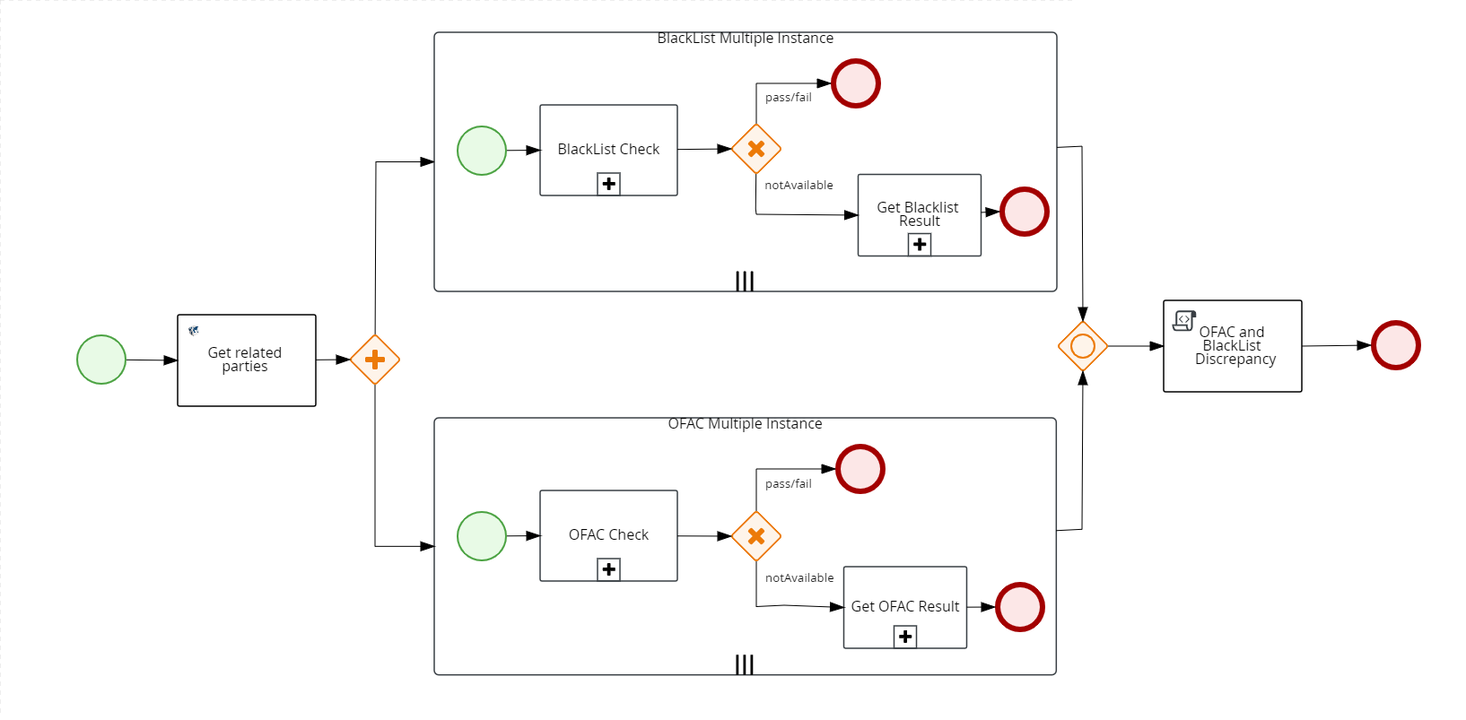

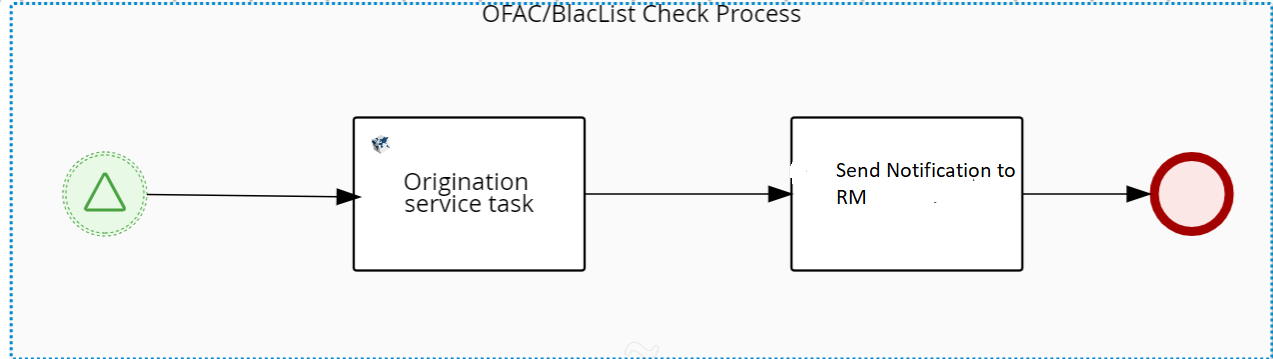

OFAC Check

The system checks if there is an existing OFAC report for the Applicant in Party MS. If there is a report that is not older than 5 days, the existing data is updated. Otherwise, if the report is older than the expected days, then a new report must be fetched from an external system and shall be stored in Party MS. The number of days (here, 5 days, is configurable from Spotlight).

Once the results are received, this task must be automatically updated with the results and closed.

Black List Check

The system checks if there is any existing Black list report for the Applicant in Party MS. If there is a report that is not older than 5 days, the existing data is updated. Otherwise, if the report is older than the expected days, then a new report must be fetched from an external system and shall be stored in Party MS. The number of days (here, 5 days, is configurable from Spotlight).

Once the results are received, this task must be automatically updated with the results and closed.

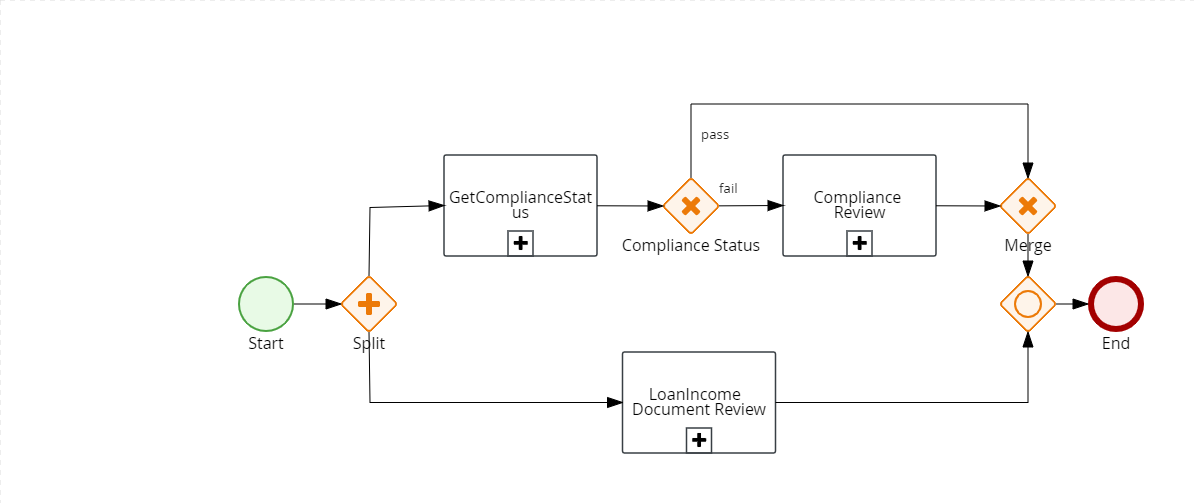

Review Compliance

If the status of both OFAC and Blacklist check is "Pass", then the Review Compliance task must be automatically closed.

The Review Loan Document, OFAC and Blacklist tasks happen in parallel.

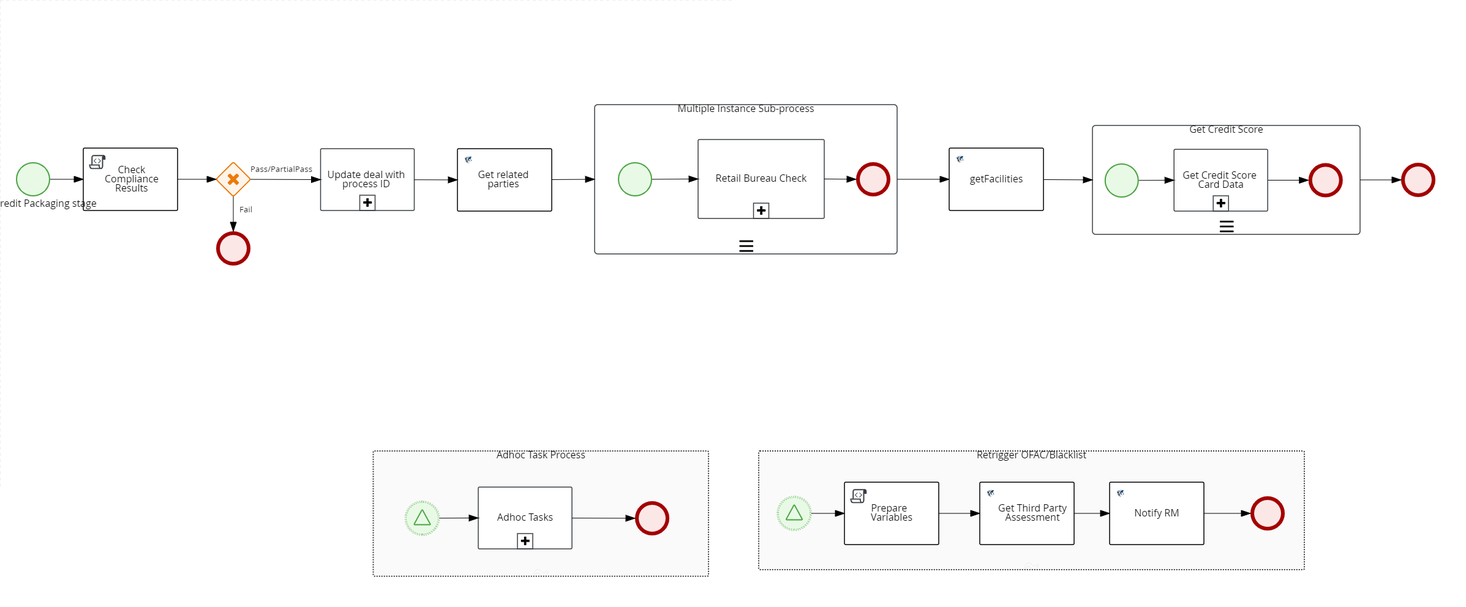

Credit Packaging

Bureau Check

If all the compliance results are Pass or if the results are Partially Pass then system continues fetching the Bureau Score. Also, the system checks if there is any existing bureau report for the applicant in Due Diligence MS for the existing party. If the report is older than the validity time (as per RETAIL_BUREAU_CHECK configuration), the new report is fetched from the external system. Otherwise, if the report is within the configured days, then the task is updated with existing data. The reports received from third-party services are stored in Due Diligence MS

A customer can have credit scores from different providers which are stored in in Due Diligence MS. The system can query the credit score based on the providers. The providers whose credit score must be fetched from Due Diligence MS can be configured from Spotlight.

The Entity Overview displays the history of credit score and the Request Overview displays the current credit score.

Get Credit Score

If all the compliance results are Pass or Partially Pass, then the system continues executing the Credit Scoring task. When the scoring is complete, the system updates the results and closes the task automatically.

Financial Spreading

Financial Spreading task is created in parallel with business bureau and business score task. The system checks the Financial Ratios Results under Entity Overview section. If the financial ratios data for the last three years is already present, then it is auto-completed.

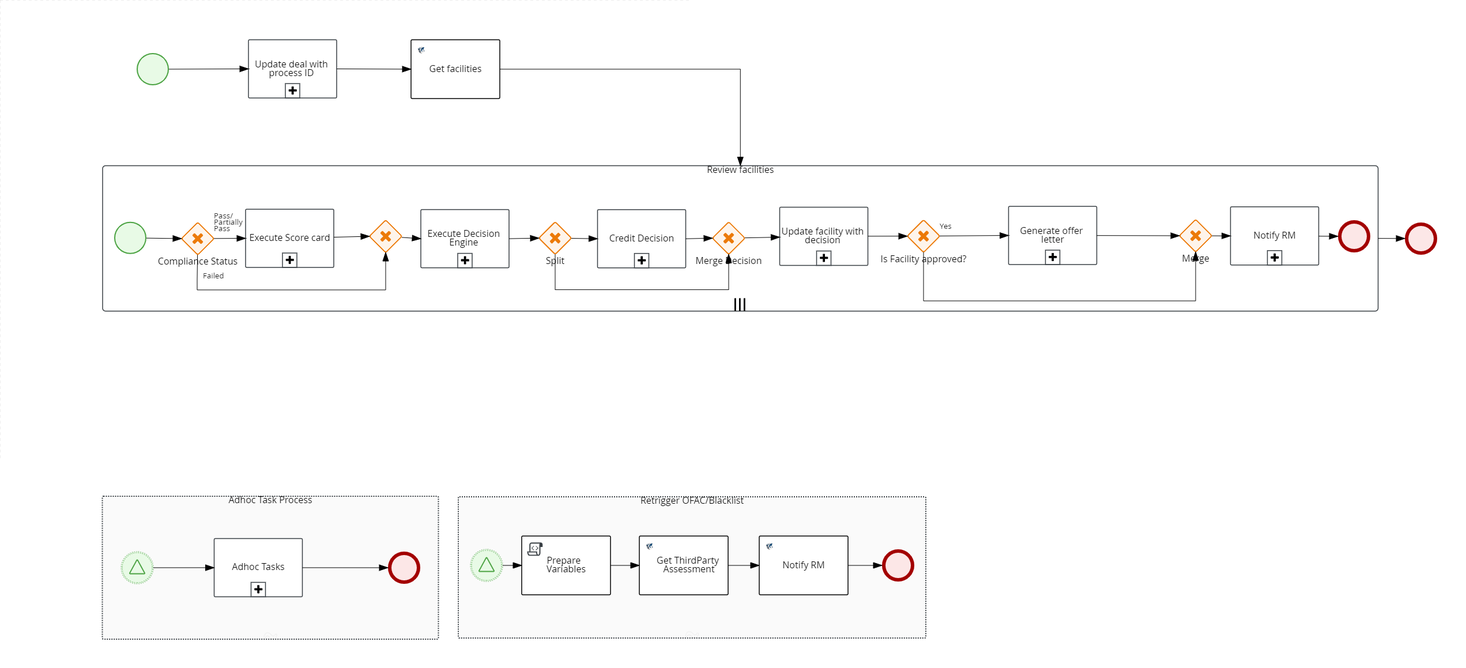

Underwriting

Decision Engine

After the Credit Scoring task is completed, the Decision engine task is triggered automatically. Based on the Decision outcome received, Decision engine task can be automatically closed. The decision can be either be Auto Approved, Auto Denied, or Manual Review.

Decision Status for the Facility is updated with the final decision if it is Auto Approved or Auto Denied.

In the Underwriting stage, a review application task is created. On completion of the Review Application task, a Credit Decision task is created for all facilities iteratively, while an Underwriter can approve or decline the request. If the credit decision task is approved, an offer letter (document generation task) is created which is an auto task by passing the transaction data to the Receipt microservice (Receipt Microservice is discontinued from 2022.04 release.The document generation capability is now handled by Formpipe,a third party tool,through Document storage Microservice). After all the required documents are generated, the Relationship Manager that claimed the application will be notified.

Review Credit Decision

The review credit decision task is created only when there is a requirement of manual decision. If the outcome of Decision Engine is either Auto Approved or Auto Denied, the review credit decision task is automatically closed.

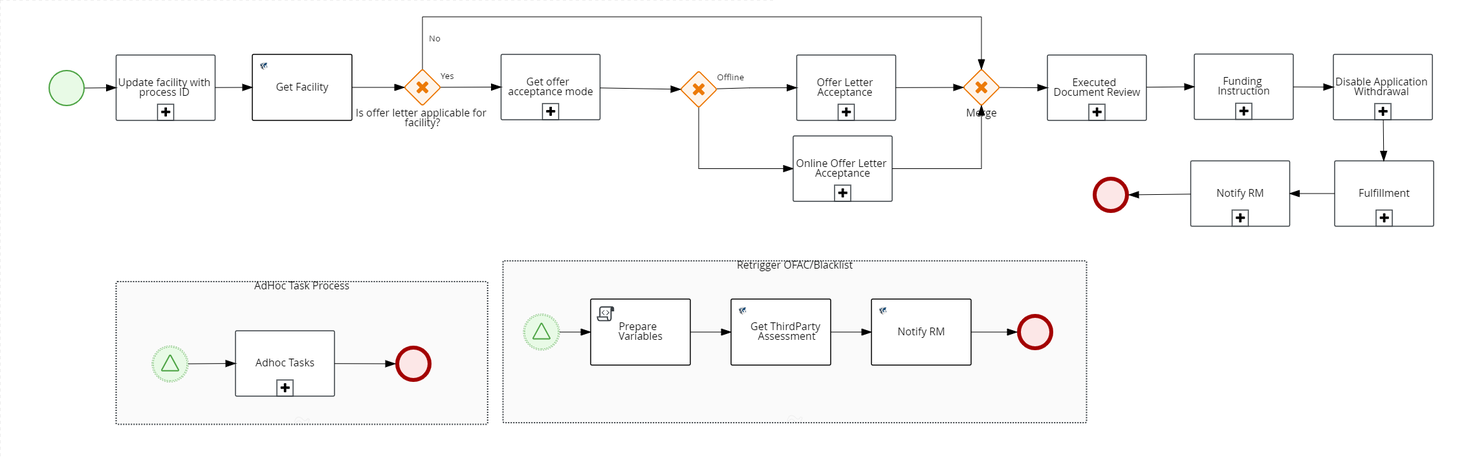

Closing

The closing stage is executed for each selected product separately.

Generate Offer Document

If the decision is marked as Approved or Auto-Approved, the offer letter document is generated. The generated offer letter is updated under the Documents section in Facility Overview.

Notification to RM: An email notification is sent to the RM after the offer letter document is generated. This task is closed automatically after the email is sent successfully.

Offer Acceptance by Customer

There are two ways of offer acceptance - Offline and Online.

The applicable offer acceptance method can be configured by using the Spotlight configuration: RETAIL_OFFER_ACCEPTANCE_MODE. The default value is Online. The value can set to Offline or Online.

- Offline: An offer acceptance task is raised and assigned to the RM to handle the offer acceptance process offline.

- Online: A customer action is raised to upload the signed document. If the customer accepts the customer action, another customer action to fetch the disbursement details from the customer is raised. After the customer action is completed, the RM manually closes the offer acceptance task. After the offer acceptance task is closed, the disbursement details are updated and the status of disbursement is Approved.

Review Executed Document

After the offer acceptance task is closed by the customer, a review executed document task is created and is assigned to Ops User. After the document is reviewed by Ops User, the task is manually closed.

Review Disbursement Instructions

After the review documents task is completed, the system checks if the status of the disbursement instructions is Approved. If yes, the system automatically closes the disbursement instructions task.

Trigger Fulfillment

Fulfillment is automatically triggered once the disbursement instructions are reviewed. This task covers the account creation as well as Loan disbursement. After the fulfillment is complete and the loan account is created, the system automatically marks the task as Completed.

Loan Completion

After the fulfillment task is completed and the loan account is created, the application is marked as Completed and this task is automatically closed.

Problem Loan Management Process

Problem Loan Management Process is enabled for the applications whose applicants are prospects and existing customers with change in customer data.

This section describes about the interventions needed manually when automating the post submission process for Retail Lending applications in Temenos Digital Assist app.

Submitted

During the post-submission flow of the Application, system will go through the following Retail Lending workflow with automated Lending process check. In the automated lending process check, the data in ODMS is compared with that of Party MS. If there is no discrepancy in address, personal, identity, income and employment information, the automated lending flow kicks in. The application is assigned to Supervisor RM and the next task is automatically processed. Otherwise, if there is any discrepancy in data, then the problem loan management flow kicks in.

Updates deal (application data) with Process ID and automated lending process check is done.

If the applicant is a prospect or an existing customer with change in KYC details (Personal, Address and Identity) and Income and Employment details, then the automated lending process task is set, and the Problem loan Management process kicks in. The application is then moved to RM Queue (Team tasks). After it is claimed by the RM user, the task is closed automatically.

Prescreening

Review KYC Evidence

KYC Evidence Review process reviews Personal, Identity and Address details of customer. For existing customers, if there is any data discrepancy, the process is initiated for RM to review. RM verifies the data manually and can again raise action if needed. Otherwise, the RM user shall close the task manually.

Review Customer

When applicants are prospects, the Applicant Review process is initiated. RM can raise a customer action if more information is needed. Otherwise, the task is closed manually by the RM.

OFAC Check

The system checks for the OFAC report. If the OFAC report status is not available/expired in Party MS, then the OFAC check is handled as in Automated Lending Process. In case of any error, an error task is raised automatically and assigned to the admin user.

Blacklist Check

The system checks for the Blacklist Check report. If the OFAC report status is not available or expired in the Party MS, then the check is handled as in Automated Lending Process. In case of any error, an error task is raised automatically and assigned to the admin user.

Review Compliance Check

Validating the OFAC and Blacklist status is handled as in the Automated Lending Process. OFAC_Status and BlackList_Status are the two output flags. If either of the two flags or both of them fails, then the Review Compliance task is created and assigned to the RM.

RM can re-trigger OFAC or Blacklist checks again by creating an adhoc task using the Temenos Digital Assist application. On clicking the Create New Task button in Temenos Digital Assist application, “Re-trigger Tasks” is added in drop-down of checklist. The status of each party compliance is updated from Compliance table of Origination Processing MS. Then the OFAC check is completed using the integration service as in the automated lending process and a notification is sent to the RM. The RM can open existing Review compliance task and check the status in task overview screen. Also, the task overview screen is updated with compliance status for each party. The Admin User can re-trigger OFAC check. The RM can also raise adhoc task to Underwriter and add comments on the Narratives tab, if necessary. After the compliance review is done, the RM can manually mark the task as complete.

Review Loan Documents

Under the Document section array of Origination Processing MS, each document status is validated. If any of the documents status from documents JSON array, is 02(Pending) or incomeEmploymentInfoDiscrepancy flag is true, then LoanDocumentReview process is initiated.

The RM can raise a customer action if any document is required or is not submitted by the customer. After receiving the information from the customer, the RM can review and raise a customer action if needed. Once done, the RM can close the task manually.

Credit Packaging

Bureau Check

If all the compliance results are Pass or if the results are Partially Pass, then the system continues fetching the Bureau Score. Also, the system checks if there is any existing bureau report for the applicant in Due Diligence MS for the existing party. If the report is older than the validity time, the new report is fetched from the external system. Reports received form third-party services are stored in Due Diligence MS. Otherwise, if the report is within the configured days, then the task is updated with the existing data.

If the report is not available, a third-party service is mocked by using a run time parameter flag (Bureau_ThirdParty). In case of any false exception, an error task is automatically generated and assigned to admin user.

Credit Scoring

If the status of all applicants is FAIL then Process is closed automatically. If all the Compliance results are Pass or Partially Pass, then the system should continue executing the Credit Scoring task.

Underwriting

Credit Assessment

Review Compliance status output is passed as input. If the status of all applicants is FAIL then Process is closed automatically.

Decision Engine

After the Credit Scoring task is completed, the Decision engine task is triggered automatically. Based on the Decision outcome received, Decision engine task can be automatically closed. The decision can be either Auto Approved, Auto Denied, or Manual Review.

If decision is Auto Denied, the “Credit Decision” process is initiated. Based on the response decision status in Temenos Digital Assist app id should be marked as Rejected and Facility stage is highlighted in red in client. The task is then closed automatically.

Review Credit Decision

Decision Engine process response is provided as input. If response is Manual Review, this process is initiated. Then a review task is raised and assigned to the Underwriter to provide the decision for facility.

If the Decision status is Denied, the status is marked as Rejected. The Facility stage is moved to Complete in the Temenos Digital Assist application, and the task is manually closed by the Underwriter.

Closing

Generate Offer Letter Document

The Decision Engine process response is input. If the response is Auto Denied, the the task is closed.

Notification to RM: The Decision Engine process response is input. If response is Auto Denied, an email is sent to the RM. The Email template, FACILITY_DENIED is used to send notification to the RM.

Offer Acceptance by Customer

The mode of offer acceptance is set through Spotlight configuration “ETAIL_OFFER_ACCEPTANCE_MODE as offline. Therefore, a manual task is raised for the RM. The RM can download the offer document, get it signed by the customer, upload the signed document in the documents section of Temenos Digital Assist application, and update the acceptance status. The RM closes the task manually.

Review Executed Documents

The Review Executed Documents task is created and assigned to Operations user. In this task, Operations user reviews the offer acceptance documents of the customer and can create adhoc task for the RM to get additional information of customer. After the offer acceptance documents are reviewed, the Operations user closes the task manually. If the customer rejects offer, the Operations user withdraws the application in the Temenos Digital Assist application and closes the task

Review Disbursement Instructions

Funding Instruction status is input. When the Funding Instruction status is Pending, a manual task is created for Ops user.

The Ops user can raise an adhoc task manually to RM, if necessary. Also, the RM can raise a customer action for the customer if more information is needed. Once done, the Ops User can close the task manually.

- Withdraw request/application: The RM can withdraw an application on behalf of a customer or prospect at any stage of the application until the limit or arrangement is created in Transact or Core banking System (CBS). After the application is withdrawn, no more user action is allowed, and the application is marked with Withdrawn status.

- All other functionality of tasks as it exists in the Temenos Digital Assist solution are available to all tasks created for retail lending requests.

- A user is not be allowed to act on a task when its dependent task is not completed.

- After the required activities for a task are complete, the user can complete the task with options as available and supported currently in the Temenos Digital Assist solution.

Stage Indicator

The stage indicator is displayed on top of the request and facility overview screens. A bank user can see the current stage of the request with status and view the tasks by clicking the View All Related Tasks link with the count of related tasks in parenthesis. The following color codes are used to indicate the status of tasks in the respective stages:

- The stage is yet to be visited.

- The tasks are in progress and one or more tasks are to be completed. The application is still in the stage.

- All tasks in the stage have been completed. The application is moved out of the stage.

In this topic